By Kyle Ramos • February 11, 2026

KYIV In the shadow of a grinding war of attrition, a different kind of conflict is intensifying within Ukraine’s borders: the battle for “industrial oxygen” ferrous scrap metal. As the nation’s metallurgical giants attempt a Herculean recovery, a growing chorus of industrial lobbyists is calling for a total ban on scrap exports.

However, a deeper analysis reveals a complex paradox. While domestic producers like Metinvest and Interpipe fear a raw material drought, many economists argue that closing the borders could backfire, stifling the very economic dynamism Ukraine needs to survive.

The Phoenix Rising: A Sector in Recovery

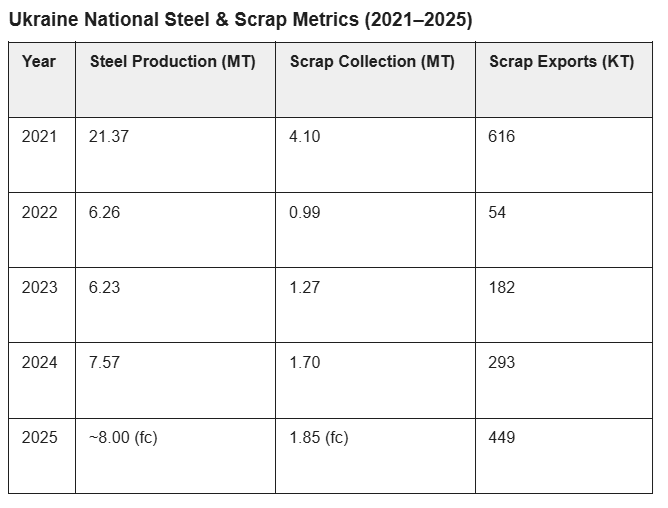

Ukraine’s steel industry, once the 13th largest in the world, was nearly extinguished in 2022. The fall of Mariupol alone wiped out 40% of the nation’s steelmaking capacity, including the legendary Azovstal works. National output plummeted from over 21 million tonnes in 2021 to a mere 6.2 million tonnes.

Yet, 2024 and 2025 have witnessed a remarkable “wartime equilibrium.

National Production: Rebounded to 7.57 million tonnes in 2024.

The Sea Corridor: The unilateral maritime route from Odesa has lowered logistics costs, allowing bulk metals to reach global markets again.

Defense Demand: The rapid expansion of UkrOboronProm has created a surge in demand for specialized armor-grade steel.

+1

The Scrap “Leakage” Controversy

The tension centers on a sharp rise in scrap exports, which hit a four-year high of 448,680 tonnes in 2025. Despite a nominal export duty of €180 per tonne, over 85% of this material is flowing into the EU primarily Poland and Greece, duty-free under the Ukraine-EU Association Agreement.

Industrialists claim this is “leakage.” They argue that Poland acts as a transit hub, where Ukrainian scrap is re-exported to Turkey. Interpipe, which operates high-efficiency Electric Arc Furnaces (EAF) that run on 100% scrap, has been the most vocal, warning of a looming deficit of up to 500,000 tonnes by 2026.

“Without scrap, the green reconstruction of Ukraine is a pipe dream,” says one industry analyst. “You cannot build a modern, low-carbon economy without the circular flow of metal.”

The Counter-Argument: Why a Ban Could Be Fatal

While the “scrap gap” sounds alarming, a total export ban risks creating a domestic monopoly that could devastate the broader economy.

The Danger of Monopsony

If exports are blocked, a handful of domestic steel majors become the only buyers. This “monopsony” allows them to artificially suppress prices. While this lowers costs for Metinvest or ArcelorMittal, it starves the scrap collection industry of the capital needed to operate.

The Cost of Collection

Collecting “war scrap” is not a simple task. Much of it is:

Contaminated: Riddled with unexploded ordnance (UXO) that requires expensive demining.

Inaccessible: Located in “grey zones” or mined territories where labor is scarce.

Bureaucratic: Destroyed military equipment is state property, involving legal hurdles to process.

If domestic prices are forced too low by an export ban, scrap yards will simply stop collecting. The result? Less scrap for everyone, not more.

Corporate Adaptations: Resilience in Action

The major players are already diversifying to mitigate these risks:

Metinvest: Having lost its Mariupol “crown jewels,” it has pivoted to its Kamet Steel and Zaporizhstal assets. It is maximizing efficiency by using its captive coking coal supplies from the Pokrovske mine.

ArcelorMittal Kryvyi Rih (AMKR): Facing a scrap squeeze, AMKR increased its pig iron production by 16.9% in 2025, leveraging its own iron ore mines to substitute scrap with hot metal.

Interpipe: Positioned as a “Green Steel” pioneer, it is banking on its low carbon footprint to maintain a premium in the EU market, even as it lobbies for tighter scrap regulations.

The Path Forward: Integration, Not Isolation

The logical solution for Ukraine lies not in protectionism, but in deeper integration with the European Union.

By maintaining an open market, Ukraine ensures that its scrap collection industry remains profitable and technologically capable of cleaning up the millions of tonnes of debris left by the war. Simultaneously, the “Green Reconstruction” provides a chance to replace destroyed Soviet-era blast furnaces with modern, scrap-intensive EAFs that align with the EU’s Carbon Border Adjustment Mechanism (CBAM).

The “battle for resources” will define 2026. If Ukraine can balance the needs of its industrial giants with the necessity of a free, competitive market, it won’t just rebuild its steel industry it will forge a more resilient, European future.